JIL’s Take on AI: Z.ai’s Landmark Listing – A Milestone for the Global AI Industry

- investment33

- Jan 9

- 3 min read

By John Ian Lau January 9, 2026

Yesterday, on January 8, 2026, Z.ai (formerly Zhipu AI, stock code 02513.HK) made history as the world’s first publicly listed company focused on large language models (LLMs), debuting on the Hong Kong Stock Exchange. Priced at HK$116.20 per share, it opened at HK$120.00, achieving a market capitalization exceeding HK$51 billion (approximately US$6.6–6.8 billion). This landmark event provides fresh transparency into the AI sector’s realities, especially in China, where Z.ai leads with its GLM series (including GLM-4.7, topping open-source benchmarks in coding, reasoning, and agentic tasks).

Why This Listing Matters: Insights into AI Monetization

Z.ai’s public debut reveals a high-burn, pre-profit reality common among frontier AI developers. In the first half of 2025, it generated around RMB 191 million (~US$27 million) in revenue—showing strong growth—but posted losses of RMB 2.4 billion due to surging R&D and compute costs (R&D expenses nearly doubled year-over-year). This high-intensity investment phase relies on API services, enterprise adoption (over 12,000 customers and 80 million end-user devices), and open-source momentum for scaling.

Monetization paths shine through cost-efficient inference, open-source leadership (GLM-4.7 ranks #1 on key benchmarks like CodeArena), and enterprise tools like the “GLM Coding Plan” and AutoGLM for agentic applications. The IPO raised over HK$4 billion (mostly for R&D), validating access to public capital via Hong Kong’s specialist tech frameworks like Chapter 18C—amid fierce competition.

Compare and Contrast with Global Competitors

Z.ai carves a distinct niche:

• Vs. OpenAI / Anthropic: These private giants boast sky-high valuations but share profitability hurdles. Z.ai’s open-source focus and lower-cost models provide accessibility advantages, particularly in emerging markets. OpenAI leads closed ecosystems; Z.ai excels in domestic chip compatibility (over 40 Chinese chips) and rapid open iteration (GLM-5 incoming).

• Vs. Other Chinese Players: Among China’s “AI tigers” (e.g., DeepSeek, Moonshot), Z.ai stands out with full-stack localization and superior coding/agent performance. Its listing paves the way for peers like MiniMax, signaling capital market maturation in China’s LLM space.

• Broader Global Context: No major Western LLM pure-play has listed yet, positioning Z.ai as a benchmark. It underscores China’s strength in open-source and speed, while U.S. firms dominate proprietary scale and funding.

Longer-Term Perspectives on Performance

Z.ai’s outlook is promising yet challenging:

• Growth Drivers: Model upgrades, API expansion, and international ties (e.g., Middle East) should accelerate revenue. IPO proceeds bolster compute and talent.

• Risks: Ongoing losses, price competition (with potential U.S. margin compression), regulatory issues (prior U.S. entity list), and compute reliance persist.

• Optimistic View: As AI evolves toward agentic/production use cases, Z.ai’s strengths suit long-term leadership in Asia and beyond.

AI vs. Dot-Com Era: Debt vs. Balance Sheet – Why We Remain Constructive

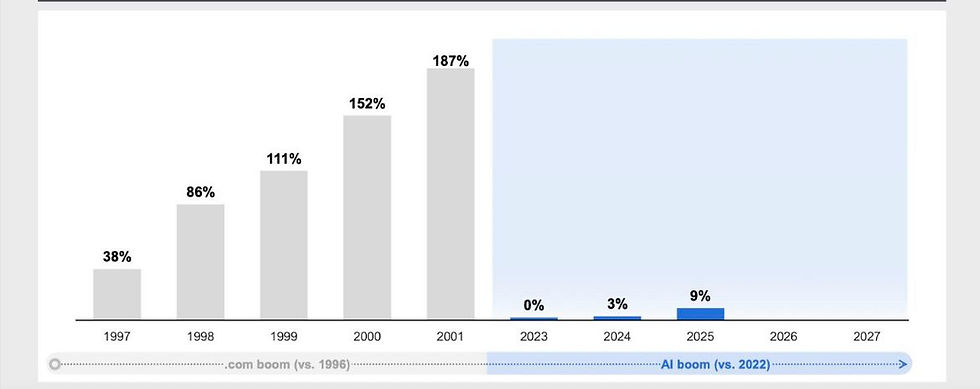

The chart below illustrates market enthusiasm: the dot-com boom (vs. 1996 baseline) saw explosive gains peaking at 187% by 2001, while the current AI boom (vs. 2022) shows modest progress (0% in 2023, 3% in 2024, 9% in 2025), with projections for 2026–2027 still in early stages.

A key differentiator: dot-com ran on debt, while AI is primarily on balance sheet. During the late 1990s, telecom/dot-com infrastructure was heavily debt-financed (e.g., WorldCom amassed $30 billion in debt before collapse; vendor financing and $300 billion+ in accumulated debt amplified the bust). Many speculative IPOs and overbuilt networks (e.g., 80 million miles of fiber, only 5% utilized) led to cascading failures.

In contrast, today’s AI infrastructure (data centers, compute) is largely funded by strong corporate cash flows and balance sheets from profitable hyperscalers (Microsoft, Alphabet, Amazon, Meta). These firms generate massive free cash flow, with most early capex from retained earnings—though debt issuance has risen (e.g., hyperscalers issued ~$121 billion in 2025, above averages, and off-balance-sheet structures appear). Overall, leverage remains contained compared to dot-com excesses, with tech leaders holding net cash positions and robust profitability.

This fundamental strength—real earnings backing investments—reduces systemic risk. Even as debt enters more (projected trillions ahead), the foundation is healthier: no widespread vendor fraud, stronger anchors, and genuine demand in a capacity-constrained market.

Sector Reassessment: Still Pro-AI, with Added Clarity

I’ve remained bullish on AI’s transformative power, and Z.ai’s listing strengthens that stance. It delivers clarity: frontier AI is capital-intensive and pre-profit, but emerging models (API, open-source, enterprise) work. No major negatives—rather, it matures the sector, draws capital, and spotlights China’s role. The hype-reality gap closes, rewarding disciplined players like Z.ai.

In summary: A landmark for AI globally. The race continues, but with stronger underpinnings than dot-com, the path to sustainable value looks clearer. We stay constructive.